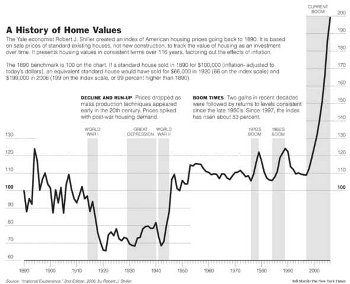

Bob Shiller’s original chart of historic home values back to 1890 was originally published in 2006. The four charts below provide an interesting perspective.

The original:

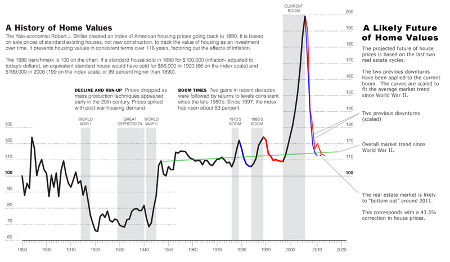

With projections overlaid:

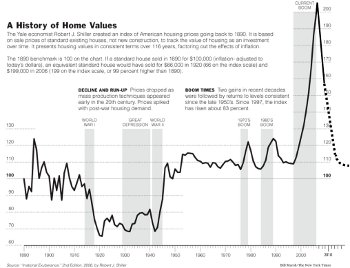

Updated, December 2008:

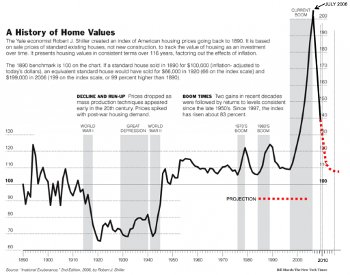

Updated, June 2009:

Bob Shiller’s original chart of historic home values back to 1890 was originally published in 2006. The four charts below provide an interesting perspective.

The original:

With projections overlaid:

Updated, December 2008:

Updated, June 2009:

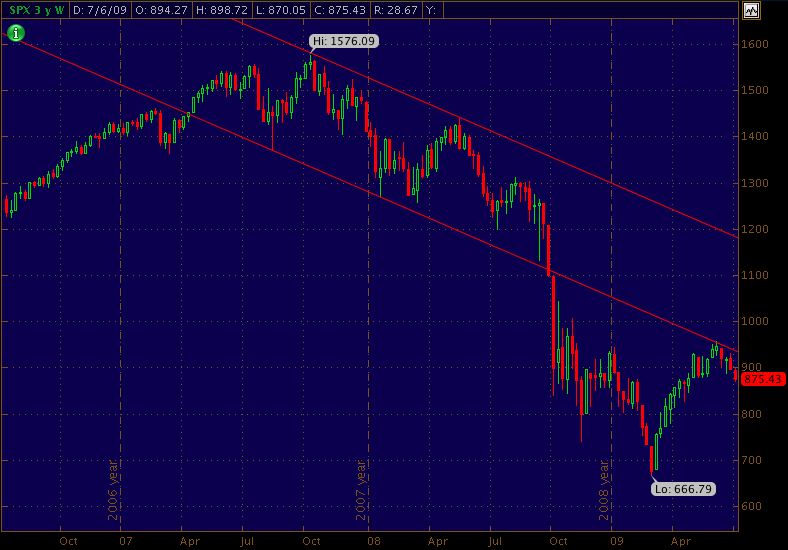

I had drawn this channel some time ago, before the June retrace. Isn’t it beautiful?

Andy Xie, writing for Caijing in early June, provided a timely warning for those attached to the recent market rally.

The Washington Post reports regulators have reached a general agreement on handling derivatives, but reveals that the administration is still woefully ignorant of the problems at hand. To wit,

Non-standard derivatives would be exempt from much of this regulation. These are derivatives linked to highly complex investments, such as securities composed of mortgages and other kinds of debt.

Broad Agreement Reached on Derivative Oversight, 2009-06-23

The word “complex” has been overused of late, just like the phrases “cash-strapped” and “unforeseeable”. It often appears when a reporter has encountered a concept requiring more than five minutes to explain and is thus beyond their understanding. Presumably it is also beyond the understanding of the reader, an assumption that likely holds in the general case but does a disservice to those members of the population retaining some minor cognitive ability. (I am unnecessarily harsh to Mr. Goldfarb, the reporter of this piece, but the opening was given. Other articles are far more deserving.)

In this case, however, the adage regarding investments that cannot be suitably explained in less that five minutes holds particularly true. Christopher Whalen, in yesterday’s testimony to the Senate Subcommittee on Securities, Insurance, and Investment, provides an excellent summary of the exploitable inefficiencies of the OTC derivatives market.

In my view, CDS contracts and complex structured assets are deceptive by design and beg the question as to whether a certain level of complexity is so speculative and reckless as to violate US securities and anti-fraud laws. That is, if an OTC derivative contract lacks a clear cash basis and cannot be valued by both parties to the transaction with the same degree of facility and transparency as cash market instruments, then the OTC contact should be treated as fraudulent and banned as a matter of law and regulation. Most CDS contracts and complex structured financial instruments fall into this category of deliberately fraudulent instruments for which no cash basis exists.

– Christopher Whalen, 2009-06-22

Mr. Whalen’s opinion is no doubt influenced by his encounters with past fraudulent practices, specifically the use of side letters in reinsurance scams. In another article, conveniently appended to the above linked testimony, he provides some history of these practices. His suggestion that AIG moved into the CDS industry as a result of greater law enforcement awareness of such side letters may not be without merit, and is certainly deserving of thorough investigation. (In this context a side letter, or email in these more modern times, is a secret agreement between two parties that effectively nullifies a public agreement. This allows a company to mislead regulators and the public about its capitalization.)

Indeed, one source with personal knowledge of the matter suggests that there may be emails and actual side letters between AIG and its counterparties that could prove conclusively that AIG never intended to pay out on any of its CDS contracts.

A few items on my mind, deserving of note: