This has certainly been an exciting week in the markets, and I’m going to need more popcorn. At times like this, people start asking questions that can generally be answered with “it’s a little too late to do anything about it”. In short, lacking a feel for the market, people tend to buy and sell at the worst possible times. What follows is my personal take on likely outcomes.

First, my price targets for the S&P 500 remain unchanged; 1070 intermediate, final bottom around 850. (The final number has a good deal of wiggle room; we could easily reach the 700s.) We should reach the final bottom in one to two years. What is most likely over the next month or two is yet another bear market rally. The second most likely outcome is a plunge down to 1070 preceding such a rally. Any move for which one is not already positioned carries sizable risk; either missing a rally or enduring another significant decline.

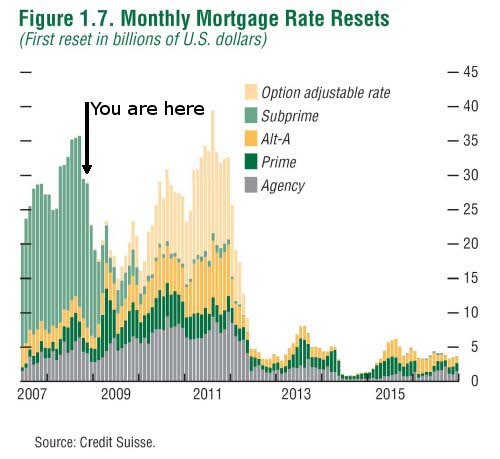

Who’s next?

My list of major financials with overexposure to toxic waste also remains the same. Some names, of course, are already out of the game.

- Ambac (crippled)

- MBIA (crippled)

Bear StearnsFannie MaeFreddie Mac

Lehman BrothersMerrill Lynch- Morgan Stanley

- Washington Mutual

- Wachovia

- Citibank

- Goldman Sachs

- Wells Fargo

This is not an exhaustive list, it does not include tech companies like Google and Apple, nor does it include automakers or companies like AIG or Capital One. My position on equities in general is that P/E ratios are too high, and that earnings estimates fail to account for current economic conditions. In short, they are still significantly overvalued.

What’s Safe?

My list of safe places remains only cash and short term Treasuries. Money market funds are not cash. Foreign economies have problems of their own.

Split your deposits between multiple banks or brokerages and stay under the FDIC limits. Don’t try to game them with PoD accounts; having access to some of your money at a separate bank is far better than potentially waiting months for the FDIC to determine that your entire deposit really is covered and that they can send you a check after all.

What Might Go Wrong?

Nouriel Roubini has a list, “The Twelve Steps to Financial Disaster“. Since its creation we’ve managed to check off a number of items on it. I still consider a severe recession the most likely outcome, but this nightmare scenario has a very real (and increasing) probability of occurring.

Update: I see the SEC is considering a ban on short selling. My first attempt to describe it resulted in some strong language which I relocated to a separate post so as not to offend those who don’t get out much.

Debunking

Finally, I’d like to address some misconceptions I’ve seen floating about the net:

1. Foreclosures are the root of the problem (Senator Dodd and others)

Foreclosures are the symptom. A housekeeper making $14 per hour cannot afford a $500,000 mortgage. When such loans are made, house prices become wildly elevated. The quickest solution to the problem requires the quick transition of such “homeowners” to rental units and a reduction in house prices to levels affordable using sound underwriting standards.

2. It’s a liquidity problem (Bernanke)

Like hell. For example, Wamu was paying dividends out of “capitalized interest”. In other words, when borrowers were making payments that did not even cover the interest portion of the loan, Wamu was booking the difference as income. For the first quarter of ’07, that phantom “income” represented nearly half of their earnings. (Wamu is not alone in this.) This is a cash flow problem.

For a second example, consider the aforementioned housekeeper having a $100K second mortgage. That is likely a total loss, yet it has been securitized, resold, and is likely sitting quietly on the books of, say, Goldman Sachs as a “Level 3 asset”, at its original $100K mark (perhaps with a 2% discount for appearances’ sake). For many companies, this will represent a solvency problem.

3. Nobody could have seen this coming (most CEOs)

Sure they did, but admitting to fraud is often a career-limiting move. Over the past few years I heard hundreds of stories about the various ways lenders and borrowers were exploiting the system to defraud investors. Investigations into the truth of the “liar loan” sobriquet only confirmed the rumors. A look at basic market fundamentals would have indicated that the price growth could only be supported by massive and systemic fraud, not to mention near-criminal negligence on the part of regulators.

4. Things might get better (average retail investor)

Take that worthless $100K and leverage it 30:1 (minimum; it could be 60:1 or even 200:1 after changing hands). That represents at least $3 million that is going to be obliterated instantly once that single mortgage is recognized as failed. Most of this damage has not been recognized, and an even greater amount of damage has yet to occur. This is why the credit markets remain frozen no matter what the administration attempts; there can be no lending without trust, and counterparty trust has completely broken down. Announcing new ways of allowing companies to hide what’s on their balance sheets does nothing to restore trust. The endgame of such a situation is collapse.

5. It’s the fault of the shorts (various CEOs, Mr. Cox of the SEC)

No. Share prices are down because the market is slowly recognizing the worth of certain companies. If the SEC did not exempt the broker-dealers (Goldman, Bear, Merrill, Morgan, Lehman) from capital requirements, they would not have been leveraged at 30 or 40 to 1. There’s a word for companies that do that, and it’s “dead”.

6. House prices will never… (NAR)

- fall nationally? Busted.

- fall in the Bay Area? Busted.

- fall in the Peninsula? Busted.

- fall in SF? Busted.

- fall in desirable SF neighborhoods? …You’d think most people would have given up at this point, but no, some people Just Don’t Get It.

There is no “massive money waiting on the sidelines”. Armies of wealthy foreigners are not going to keep prices up. And no, there is no Santa Claus.