Introduction & Recent News

“Only when the tide goes out do you discover who’s been swimming naked.”

— Warren Buffett

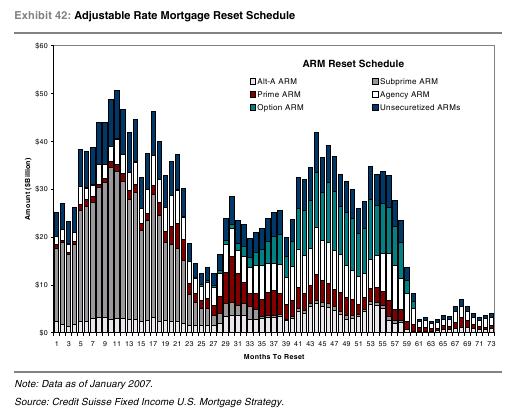

This post is on recent developments in the finance world. I’ll start things off with a small chart, courtesy of Credit Suisse, then explain its connection to imploding hedge funds.

Note that the pipeline holds a significant volume of loans, over a trillion dollars in total, with 500 billion dollars for 2007 alone. Those interested in the gritty details may review the entire report. Suffice to say, the quality of these mortgages underlies an assortment of financial instruments which may be passed on to other investors, be they hedge funds, banks, or pension funds. The value of these instruments is a bit, in the words of one participant, theoretical.

In late June, Brookstreet Securities in Southern California saw its capital fall from $16 million to -$3 million when the value of the CMOs (Collateralized Mortgage Obligations) it held were “marked to market” at a price of 18 cents on the dollar. Some customer accounts “did indeed go negative”.

Remember Brookstreet, the brokerage whose overleveraged retail clients discovered the magic of mark to market a while ago? Evidently the SEC is interested in exactly how that went down. Stories are being, well, not exactly stuck to yet. They’re in the works:

[Stanley Brooks] said he is still trying to sort out how the firm imploded. “It’s so complicated that the smartest guys in the industry got their lunch handed to them,” he said. “It was a perfect storm.”

– Tanta, on the blog Calculated Risk

Brookstreet was not the only casualty. Two hedge funds at Bear Stearns, controlling over $20 billion just a few weeks prior, found their investments in CDOs (Collateralized Debt Obligations) similarly reduced. Bear Stearns was able to prevent total collapse by negotiating deals with most creditors. Ironically, Bear Stearns refused to take part in Wall Street’s multi-billion dollar bail-out of LTCM back in 1998, so it is likely with some pleasure that Merrill Lynch seized about $850 million of the funds’ assets to sell at auction.

There is more to the ARM reset schedule than is immediately apparent. Certain characteristics of recent loans make them extremely vulnerable to a reset, chief among them being borrowers qualified based on initial teaser rates, and extremely high debt-to-income ratios. For a significant percentage of loans, the reset schedule effectively models delinquencies.

According to our contacts, homebuyers were primarily qualified at the introductory teaser rate rather than the fully amortizing rate, which for many buyers was the main reason they were even qualified in the first place.

– Credit Suisse, “Mortgage Liquidity du Jour: Underestimated No More”

Ratings and Quality

Cash flows from the loans (or bonds, or even other CDOs) that comprise a CDO are split into classes called “tranches” based on priority of payments; referred to (in order of increasing risk and yield) as senior, mezzanine, and equity. CDOs will be rated by agencies such as Moody’s, Fitch, or S&P. In theory this allows some determination of investment quality. CDOs are complicated, and dangerous. To quote Tanta again,

Buying a B tranche of a subprime ABS is playing with matches. Buying the equity tranche of a CDO is playing with a blowtorch in the parking lot of the Exxon station while wearing a St. Lucia wreath on your head.

– Tanta, after noticing such tranches being sold to pension funds

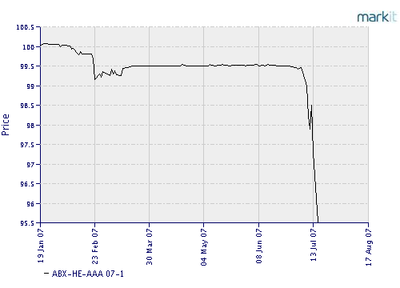

While delinquencies in subprime space have been disturbingly high for many months, many of these instruments maintained their investment-grade ratings. Agencies responded to critics by saying they were waiting until foreclosure sales proved a sufficient decline in the value of the underlying assets. They also note that the available data may not be of the highest quality:

“Data quality is fundamental to our rating analysis,” S&P said. “The loan performance associated with the data to date has been anomalous in a way that calls into question the accuracy of some of the initial data provided to us.”

Part of the problem may also lie in the methodology used to assign ratings, as illustrated in this talk by Robert L. Rodriguez of First Pacific Advisors:

We were on the March 22 call with Fitch regarding the sub-prime securitization market’s difficulties. In their talk, they were highly confident regarding their models and their ratings. My associate asked several questions.

“What are the key drivers of your rating model?”

They responded, FICO scores and home price appreciation (HPA) of low single digit (LSD) or mid single digit (MSD), as HPA has been for the past 50 years.My associate then asked, “What if HPA was flat for an extended period of time?”

They responded that their model would start to break down.He then asked, “What if HPA were to decline 1% to 2% for an extended period of time?”

They responded that their models would break down completely.He then asked, “With 2% depreciation, how far up the rating’s scale would it harm?”

They responded that it might go as high as the AA or AAA tranches.– Robert L. Rodriguez, “Absence of Fear”

It appears that this is happening even now, as this chart reveals:

More recently, in a move described as a death warrant for the subprime industry, agencies have announced that they will review and lower ratings on a number of mortgage-backed securities.

Containment

A word often seen in reference to the subprime meltdown is “containment”. Like with previous references to a “soft landing”, the idea that the problems are confined to subprime is becoming very important to some people, in much the same manner that containment was very important to the crew of the Starship Enterprise.

In my own opinion, containment is a illusion. The amount of leverage in the system, from the initial home loans to CDOs comprised of CDOs built on yet another layer of CDOs (I kid you not), is unprecedented. Now that house price appreciation has effectively peaked, and the valuation models begin to break down, the main event can begin.

As mentioned before, these corrections can take many years to play out. The bulk of the Alt-A resets should not occur for another two years, unless of course the homeowner was making minimum payments. However, this correction has surprised many with its speed, and some sort of credit event before October would not be surprising.

This should not be considered investment advice. I (regrettably) have no position in BSC, MER, or any of the mentioned rating agencies as of this writing.